16 / 84

16 / 84

North America 2018

14 \

World Cement

the around 7% growth of the infrastructure segment

(considering roads and highways only). The cost of building

has also increased: private housing permits in units

increased by 6% CAGR in the 2012 − 2017 period, whereas

in US dollar terms growth was three times higher.

Rated D+ by the American Society of Civil Engineers,

road infrastructure is in dire need of rehabilitation. The

issue is not lost on the Trump administration, which has

made the country’s “crumbling infrastructure” an aspect

of its campaign. Long anticipated, the administration’s

US$1.5 trillion plan is also surprisingly hands-off from a

federal perspective. The plan, deemed a “hocus-pocus”

plan by Kevin DeGood, Director of Infrastructure Policy

at the Liberal Centre for American Progress thinktank,

assumes that a US$200 billion federal investment would

lead to an extra US$1.5 trillion from the private sector,

and from the city and state level.

It is noteworthy to mention how the needle moved

in terms of infrastructure spending in 2017: investments by

US municipalities in infrastructure stood at

US$50.7 billion in the first seven months of 2017, lower

by almost 20% year-on-year. This clearly shows that

infrastructure spending has to be funded more substantially

from the federal level. This reality is hard to conceive,

given that national debt has topped US$1 trillion and the

government had to bump up against its borrowing limit a

month earlier than expected.

The future for US cement manufacturers

This leaves cement manufactures with some confidence

in short-term opportunities only. In 2017, demand for

cement improved by 2.4% year-on-year, a marginally more

solid growth than the 1.7% growth of 2016, but below

the 3.4 and 8.0% year-on-year growth rates for 2015 and

2014, respectively. Were it not for residential construction,

2017 could have ended with a marginal 0 − 0.5% growth,

or even on the negative side. Hurricanes Harvey and

Irma, coupled with wildfires and an early on-set of

winter did little to deter growth, with demand in the

January − November 2017 period up 3.6% year-on year

(in Texas and some Southeastern states, demand fell

below historical levels in September).

The US Southeast and Pacific West regions saw the

largest CAGR growths in the 2012 − 2017 period, with

5.7% and 8.5% respectively. In contrast, demand in

the Northeast fell by 2% in the same period. The latter

region is also the one most in need of public funding

for infrastructure rehabilitation. Out of the top 10 states

that are most in need of reformation, eight states are in

the Northeast. However, that is not to say that the dire

situation of the region’s infrastructure will readily lead

to a boom in cement demand. The Northeast is likely to

be bypassed by the infrastructure investments, as critics

are quick to point out that investments will be focused in

Trump-friendly states in the South and Southeast.

Just like the country’s economy, growth in cement

consumption is steadily declining. If in the 2012 − 2017

period demand improved by 3%, the team at

CW Research forecast a below 3% CAGR growth for the

2017 − 2022 period, and below 2.5% growth in per capita

terms.

Net trade will see a much smoother growth compared

to the rapid acceleration observed in the 2012 − 2017

period. Imports will continue to be essential in meeting

demand, but CW analysts foresee domestic producers

improving their ability to keep up with the growth rate

of consumption. So far, only a handful of plants have yet

to convert from wet clinker production to dry. In 2017,

LafargeHolcim in Ravena, New York, and Oklahoma

completed two such conversions.

According to equipment suppliers to the US market,

there are quite a few mothballed operations across the

nation’s geographies. Even if demand were to grow, there

is no need for new integrated capacity (which is very

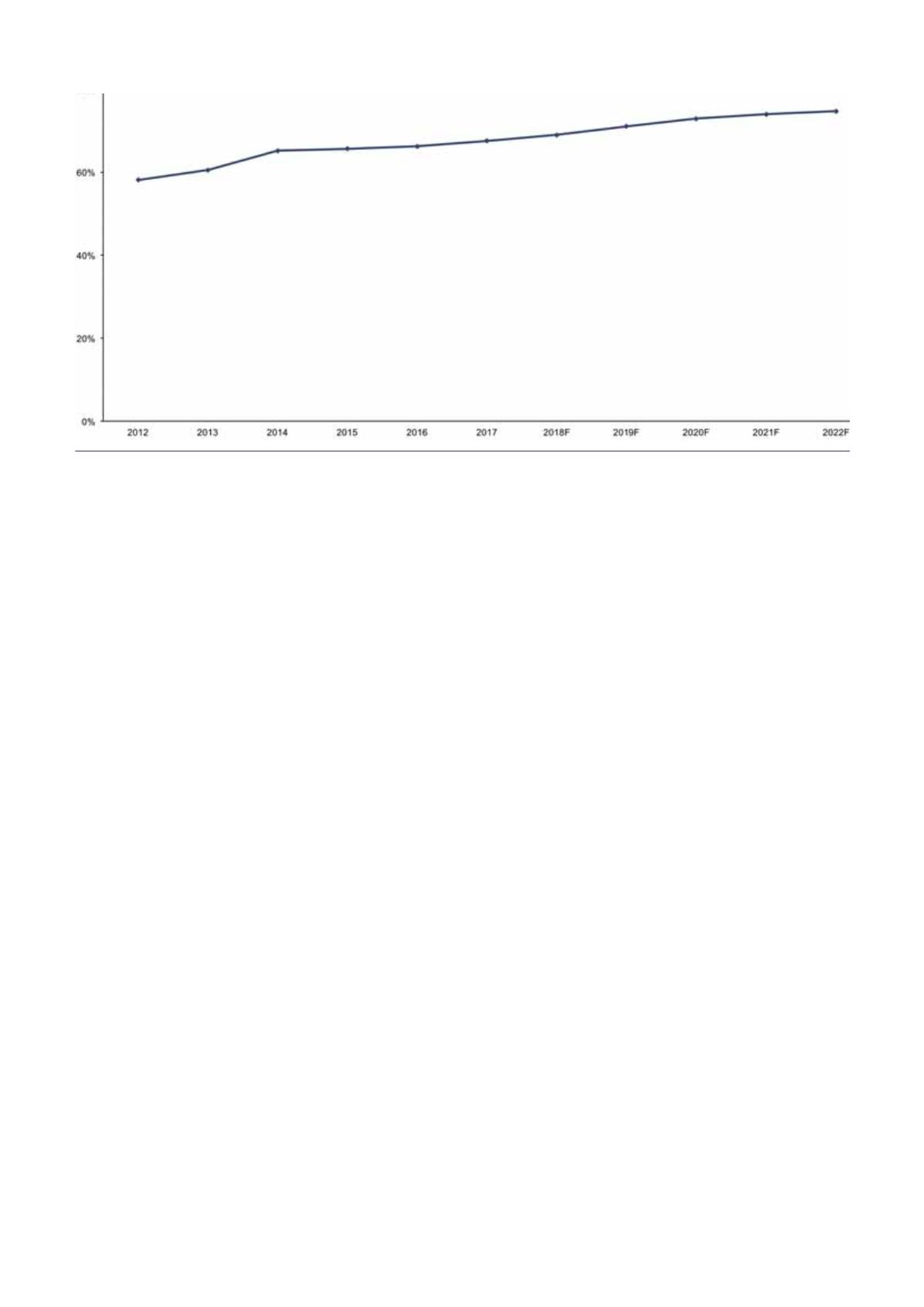

US cement utilisation rates (%).

Source: CW Research’s Global Cement Volume Forecast Report, 1H18.