18 / 84

18 / 84

North America 2018

16 \

World Cement

difficult to launch even with the current administration’s

more open environmental position).

Improving capacity

That is not to say producers are idling: almost all US

cement manufacturers are engaged in either a small

or large-scale activity, meant to optimise cement

manufacturing, that translates into heightened

environmental compliance, control, or addition of some

small extra production capacity. Environmentally, even if

the US Environemtnal Protection Agency’s stance is more

relaxed, manufacturers are well aware that it is from

the local communities that they have to gain the seal of

approval.

In the near future, CW Research expects that adding

more capacity will happen rather unconventionally.

Looking at recent attempts to enhance capacity in the

conventional way in the US, they are either trapped in

year-long hearings and debates that end up dissuading the

potential investor, or stopped before construction by local

communities. Historically, such has been the case for Titan

Cement in North Carolina, LafargeHolcim in New York,

Grupos Cimentos Chihuahua in NewMexico, and most

recently, Ecocem’s plans in San Francisco.

Adding new capacity is likely to happen through mobile

grinding plants installed at sea or rail terminal location.

Though there are no such pieces of equipment in the

US (most recently, there have been some small capacity

grinding plants installed at terminal level, but not mobile

ones), all market indicators point to the benefits of such

equipment. Importing clinker from abroad is easier and

cheaper than ever, to both the West and East Coasts, as

sources become more and more diversified. Manufacturers

in the US are largely part of international groups that can

easily use trading networks to connect to the US, meaning

sub-regional consumption hotspots are shifting quicker

than ever.

New capacity, however, is not a priority for North

American producers, which are trying to limit CAPEX

and increase pricing to bring profits back to healthy

levels. That also explains why 2017 was an eventful

year in terms of mergers and acquisitions. CRH sold its

distribution business, but is frontrunner to buy Suwannee

American Cement from Votorantim and the privately-held

Ash Grove Cement. HeidelbergCement sold its stake in

Lehigh White Cement, but purchased seven quarries and

three ready-mix plants in the Northwest from CEMEX. The

Turkish Cimsa, which exports white and gray cement to

the US, launched a subsidiary that enables its to bypass

third parties in distributing its products. Cementos Argos,

after a buying spree in the US in the last couple of years,

emerges as a dominant player in the Southeast.

Most companies in the US increased their ex-works

pricing for cement in 2017, but not only because of the

foundation provided by growing demand. Input costs of

coal, petcoke, and freight saw an uptick during the year.

The healthy EBITDA growth all US cement operations

witnessed during the year would have likely been offset

were it not for the price growth strategies adopted by

manufacturers.

Conclusion

If anything, 2018 already seems to be a more turbulent

year than 2017, but CW Research expects that the

cement sector will have to absorb fewer shocks than it

has had to in the past. Despite the controversy around

the infrastructure plans, CW Research argues that at

least a small fraction of them will start in 2018, even if

only due to populist reasoning. The backbone of the

industry, however, will not be made out of infrastructure

projects, but in the residential sector that will continue

to take the lead, supported by favourable interest rates

and single-family construction. Looking at the evolution

of demand long term to 2050, CW Research anticipates

that consumption per capita will plateau and moderately

decrease, in an indirect relationship to the positive

growth of GDP per capita.

About the author

Raluca Cercel is a Senior Analyst and Consultant responsible

for various ongoing research activities. Cercel works on

consulting projects, multi-client studies, and various key

initiatives, including global market price assessments and

market intelligence activities. Cercel holds a degree in

International Relations and a Masters in Transatlantic Studies

from Babes-Bolyai University in Romania.

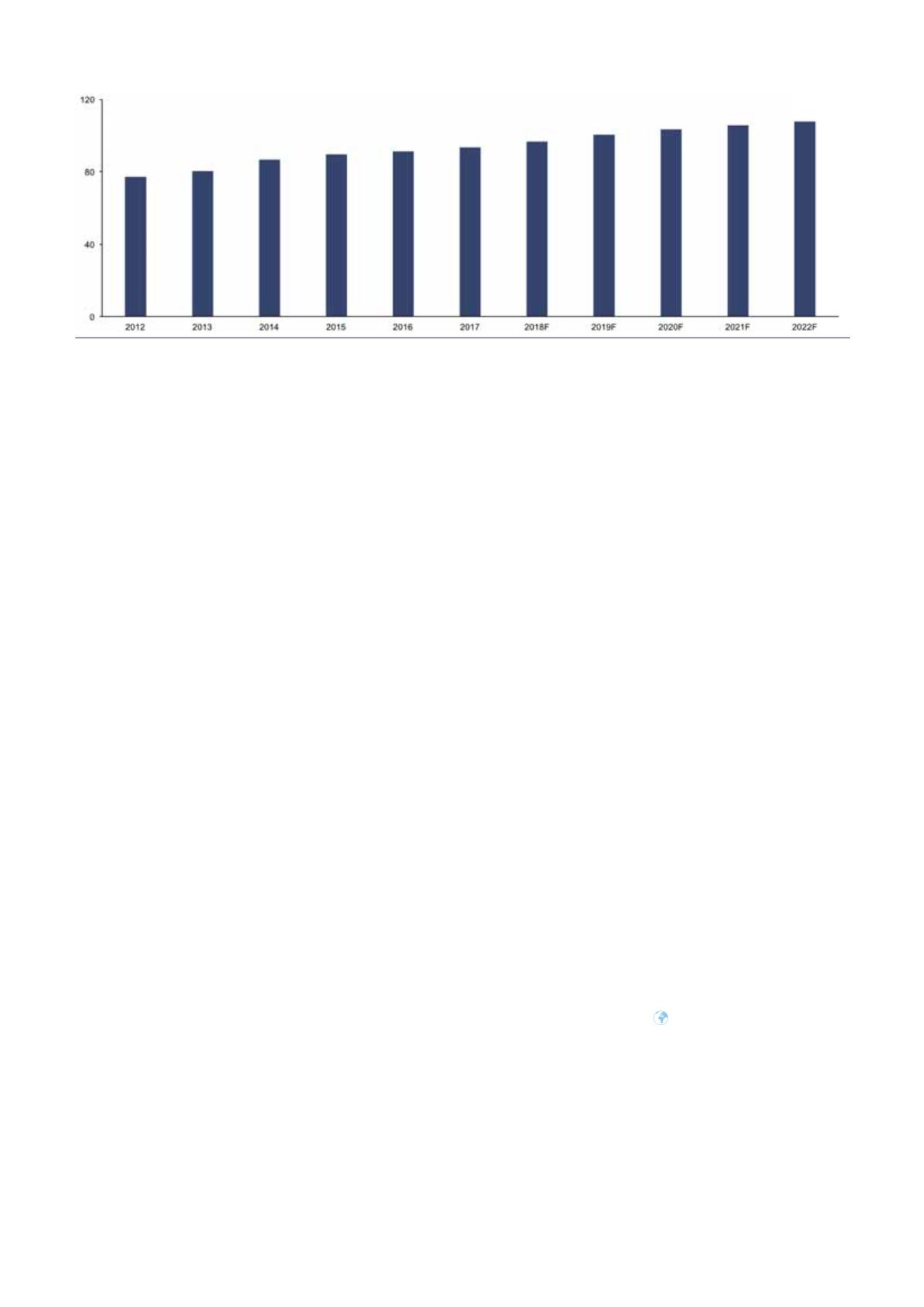

US cement demand (million t).

Source: CW Research’s Global Cement Volume Forecast Report, 1H18.