18 / 60

18 / 60

16

World Cement

North America 2019

to spend more on infrastructure. This segment,

while strong, is facing competition from health

and pension costs for public workers. In

some cities, the unfunded plans will be large

enough to bankrupt the area. If states could go

bankrupt, the US would add a few. With a new

Congress, there is an increased probability of

more federal money for infrastructure projects

(even though its chances of passage remain

below 50%). Overall, the outlook remains

good, with excellent pricing power and modest

volume growth.

State by state outlook (Figure 11) shows

modest gains for most states. North Carolina,

a strong growth state, is unusual because

SCMA shows a decline over five years – the

explanation is a very high starting point in 2018

and 2019. Most of the Northeast and much

of the Midwest will be down as out-migration

accelerates towards the warmer states.

Because SCMA believes oil prices will remain

in the US$45 to US$65 range, the Southern,

lower energy drilling cost states do well.

US cement supply outlook: 2019 to

2024

An integrated North American market

The 2020 − 2024 US supply outlook

encompasses all currently operating US

portland cement manufacturing locations,

as well as those facilities located in Canada

and Mexico that are permanent or ‘structural’

elements in the US supply equation.

z

z

Virtually all Canadian portland cement

manufacturers operate permanent facilities

in the US and product flows seamlessly

into neighbouring US market areas.

z

z

The newest cement manufacturing location

in North America, the McInnis plant

in Port Daniel, Quebec, supplies two

large, state-of-the-art marine terminals in

Providence, Rhode Island and New York,

New York.

z

z

Mexican producers GCC and CEMEX,

which both have extensive US-based

operations, regularly distribute cement

from Mexico in Texas and, less frequently,

Arizona.

Methodology and assumptions

Nameplate capacity

The starting point for the analysis is the

calculation of ‘nameplate capacity’ for all

plants serving US customers. Daily clinker

capacity (tpd) is used as reported by the

Portland Cement Association, multiplied by

330 days, and then multiplied by 1.05 for

gypsum additions. Clinker grinding capacity is

not explicitly considered in this analysis.

Clinker factor and supplementary cementitious

materials

The practice of adding ground limestone to

ground clinker to effectively increase cement

capacity is well established in Canadian

markets and should become a more common

practice in US markets in coming years. This

can lower producers’ costs/tonne of finished

cement, as well as lower the CO

2

footprint

of the finished product. Because of the

uncertainty surrounding the adoption of this

Figure 12. US portland cement supply vs

demand.

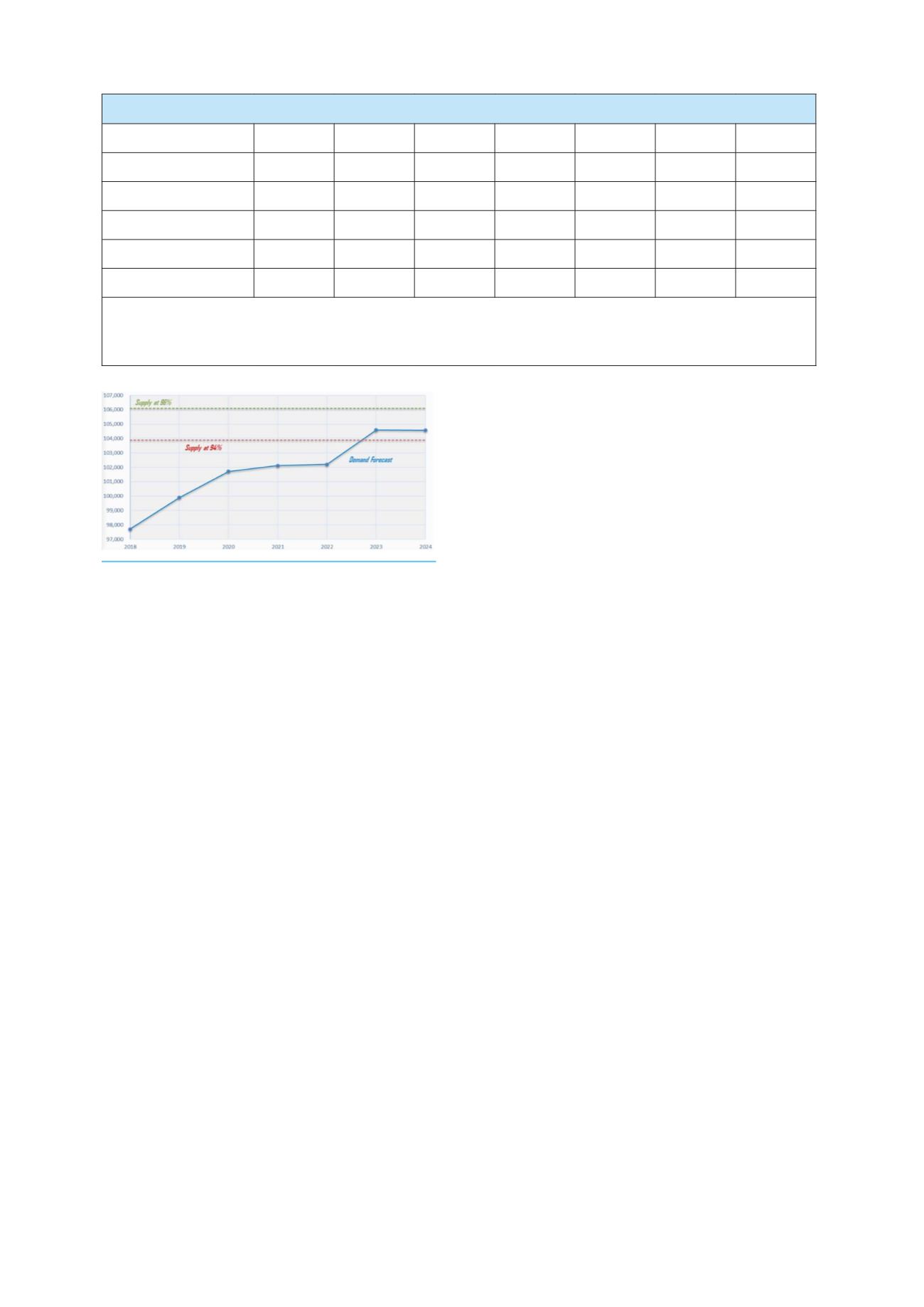

Table 1. Cement demand: baseline (million t).

2018

2019

2020

2021

2022

2023

2024

Residential

25.9

27.3

26.9

27.6

28.8

30.3

30.3

Non-residential

29.6

29.6

29.3

29.5

29.0

29.2

28.8

Non-building

42.1

43.1

45.6

45.0

44.3

45.1

45.5

Total

97.6

100

101.8

102.1

102.1

104.6

104.6

Year-on-year change (%)

+3.6

+2.5

+1.8

+0.3

+0.0

+2.4

0.0

Note: SCMA’s definition of cement is portland and blended in tonnes.

Note: There is a small difference between SCMA’s estimates of consumption and the USGS because of SCMA’s own estimates in

states where USGS does not report values due to competitive concerns.